Look, even in this digital age where everything’s about apps and instant transfers, plenty of us still rely on good old-fashioned checks for things like paying rent or donating to a cause. But what happens when a check goes missing, or you spot a mistake after you’ve sent it off? That’s when canceling it—technically called a “stop payment”—comes into play. It basically tells your bank to block the check from being cashed or deposited, saving you from potential headaches. I’ve been there myself once or twice, and trust me, acting fast makes all the difference. In this guide, I’ll break it down for you clearly, covering the why, how, and what to watch out for, so you can handle it without stress.

Why You Might Need to Cancel a Check

First things first: canceling isn’t the same as voiding. Voiding is when you scribble “VOID” on a check you haven’t used yet to make it worthless. Canceling is for checks you’ve already written and handed over, but they haven’t hit your account. Reasons pop up all the time—like if the check gets lost in the mail, stolen, or you realize you put the wrong amount or name on it. Maybe there’s a disagreement with the person you’re paying, or the deal falls through. Whatever the case, if the check’s already been processed, you’re out of luck on canceling. So, always check your account first to see if it’s cleared.

The Steps to Get It Done Right

Don’t drag your feet here—the sooner you act, the better your chances. Most banks give you a decent window, but delays can mean the check slips through. Here’s how to tackle it:

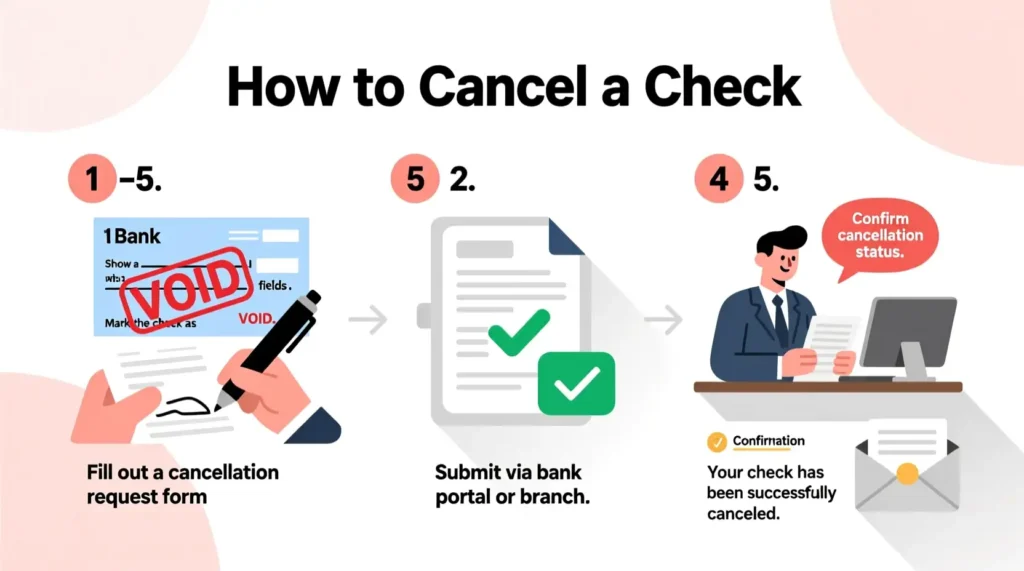

1. Double-Check If It’s Already Gone Through

Jump online to your bank’s website or app and scan your transactions. Find the check number and see if it’s posted or still pending. No sign of it? Great, you’ve got time. If it’s already deducted, though, you’ll have to sort it out with the recipient directly—maybe ask for a refund or something similar.

2. Round Up the Key Info

To make things smooth with your bank, jot down these details beforehand:

- Your account number.

- The check’s number (grab it from your checkbook or recent statement).

- The exact dollar amount you wrote.

- Who it’s made out to.

- The date you issued it.

- And if they ask, a quick explanation why you’re stopping it.

Having this ready saves time and cuts down on back-and-forth.

3. Reach Out to Your Bank

Get in touch right away. Banks make this pretty easy these days:

- Online or via app: A lot of places like Chase or Wells Fargo let you do it yourself in the app under something like “Account Services” or “Stop Payment.” Just follow the steps—it’s usually quick.

- By phone: Call their customer line; they’ll walk you through it after verifying who you are.

- In person: If you’re old-school, head to a branch, but it might take longer.

- Other ways: Some still take faxes or mailed forms, but that’s rare now.

Once it’s in, the stop payment kicks in almost immediately and typically lasts six months to a year. If the check shows up later, you might need to extend it. For cashier’s checks—those guaranteed ones from the bank—it’s trickier; you could need to file a lost check claim or even get a bond, and it might take weeks.

4. Handle the Fee and Grab Proof

Banks charge for this, usually $25 to $35—check with yours, as some waive it for certain accounts. Once paid, ask for confirmation: an email, reference number, or whatever they offer. Keep it filed away in case issues crop up later.

One thing to note: this doesn’t cover electronic stuff like ACH pulls; those need their own process.

Things to Keep in Mind and Watch For

It’s not always airtight—banks do their best, but if the check gets through anyway, they’re not on the hook. So, keep an eye on your statements. Legally, you’re good to request this under standard banking rules, but if you just say it over the phone without following up in writing, it might only hold for a couple weeks.

Also, think about the other side: let the payee know what’s up to avoid awkwardness, and suggest another way to pay them. It keeps things civil.

Smarter Ways to Skip the Hassle Altogether

Why deal with this if you can avoid it? Switch to digital where possible—Zelle, Venmo, or your bank’s bill pay service are faster and easier to track. Cards give you built-in protection for disputes too. If you must use checks:

- Proofread everything twice before sending.

- Use tracked mail for big ones.

- Go for checkbooks that make copies automatically.

- Review your accounts regularly.

Little habits like these can save you a ton of trouble.

Wrapping It Up

Canceling a check is straightforward once you know the drill, but speed and accuracy are your friends. If anything feels off, just call your bank—they’re pros at this. In our busy world, tools like this help you stay in control of your money. For specifics on your bank’s policy, give them a shout. Here’s to fewer financial surprises!